Introduction

Repossession is one of the most stressful financial situations an individual can face. Whether it involves a vehicle, equipment, or other financed assets, the threat of repossession often signals deeper cash-flow challenges rather than poor judgment or irresponsibility.

If you are asking, “How can you stop repossession?”, the good news is this: repossession is often preventable, especially when addressed early and strategically.

From a CEO mindset, repossession is not a personal failure—it is a liquidity and risk-management issue. And like most operational risks, it can be mitigated with the right actions, communication, and planning.

This guide explains how repossession works, what options are available, and how to approach the situation with clarity and control.

Understanding Repossession

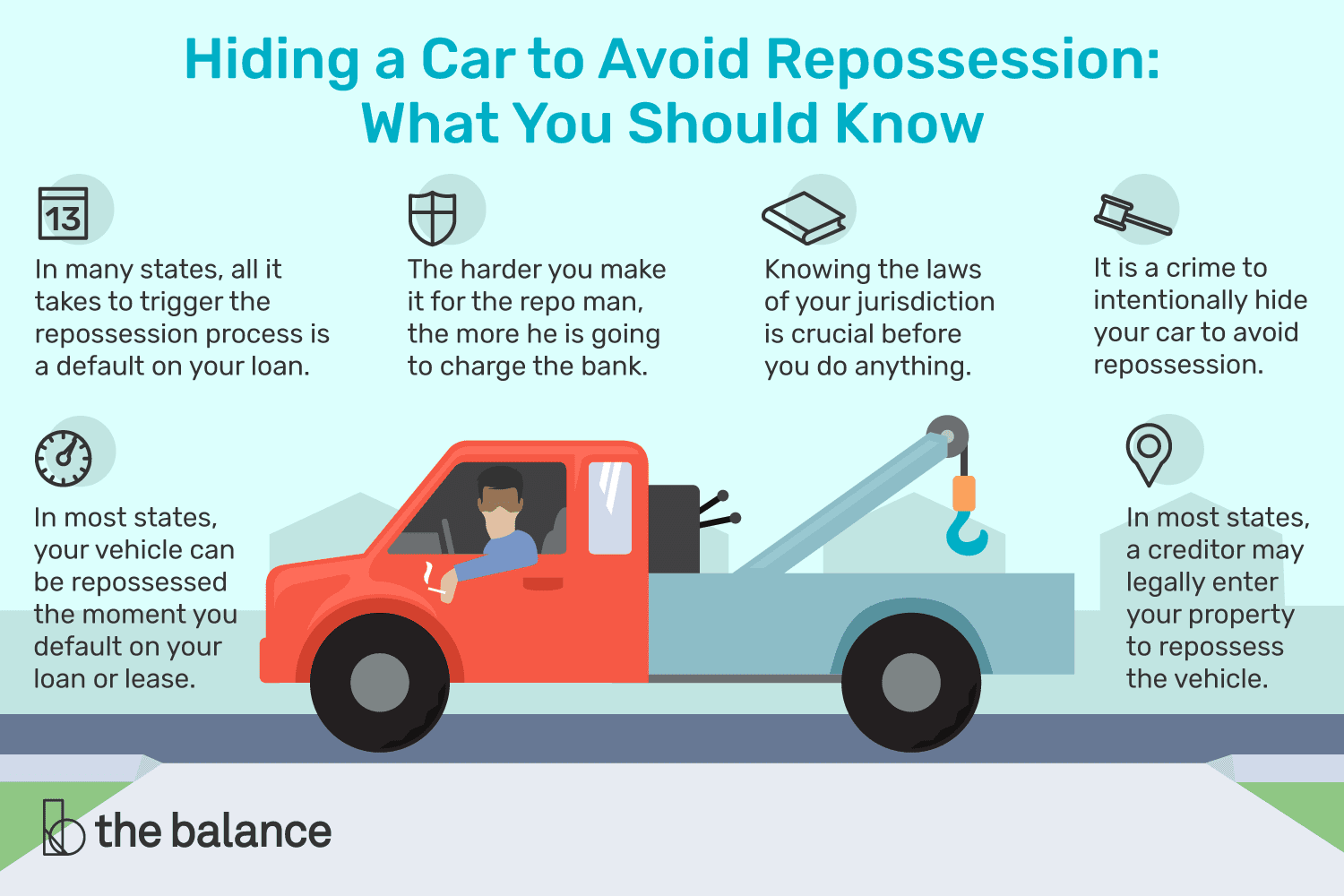

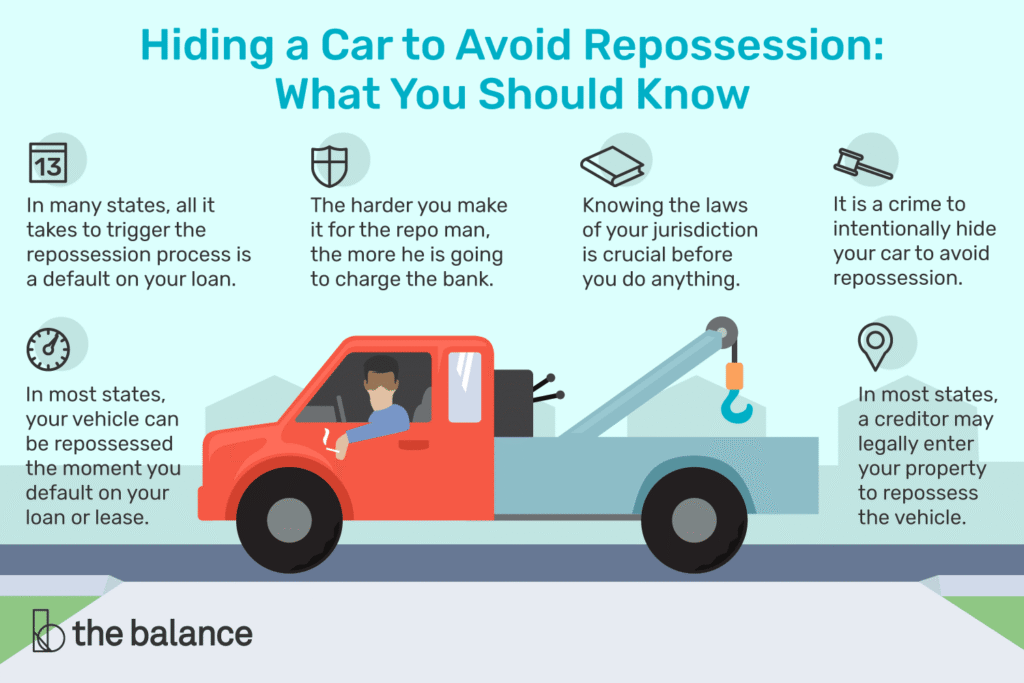

What Is Repossession?

Repossession occurs when a lender takes back property used as collateral for a loan after the borrower fails to meet payment obligations. Most commonly, this involves:

- Vehicles

- Motorcycles

- Boats

- Business or personal equipment

In many cases, lenders do not need a court order to repossess, provided they follow local laws and contract terms.

Why Repossession Happens

Repossession usually results from:

- Missed or late payments

- Reduced income or job loss

- Unexpected medical or family expenses

- Poor cash-flow planning

- Temporary financial disruptions

Importantly, repossession is often the final step, not the first. This means there is usually time to intervene.

Why Acting Early Matters

Time Is Leverage

The earlier you act, the more options you have.

Before repossession occurs, you may be able to:

- Negotiate payment terms

- Delay action

- Reinstate the loan

- Protect your credit profile

Once repossession happens, costs increase and options narrow.

Repossession Is Expensive—for Everyone

Lenders prefer repayment over repossession because:

- Repossession costs money

- Assets depreciate

- Resale values are uncertain

This creates room for negotiation if you communicate proactively.

Step One: Assess Your Financial Position

Identify the Core Problem

Before contacting your lender, understand:

- Why payments were missed

- Whether the issue is temporary or long-term

- How much you can realistically afford now

This clarity improves credibility and negotiation outcomes.

Review Your Loan Agreement

Your contract outlines:

- Grace periods

- Late fees

- Reinstatement rights

- Default timelines

Knowing these details helps you avoid surprises and missed opportunities.

Step Two: Communicate With the Lender Immediately

Why Silence Makes Things Worse

Avoiding calls or notices signals risk to lenders. Proactive communication signals responsibility.

Contact your lender as soon as you anticipate difficulty—not after repossession is scheduled.

What to Say (and How to Say It)

Approach the conversation professionally:

- Acknowledge the missed payment

- Explain the situation briefly

- Propose a realistic solution

- Ask about available hardship options

Lenders are more receptive to borrowers who engage early and honestly.

Step Three: Explore Repossession Prevention Options

Loan Reinstatement

In many cases, repossession can be stopped by paying:

- Past-due amounts

- Late fees

- Reinstatement costs

This brings the loan current and restores normal payment terms.

Payment Extensions or Deferrals

Some lenders may:

- Extend the loan term

- Allow skipped payments

- Temporarily reduce payment amounts

These options can stabilize cash flow during short-term hardship.

Loan Modification

If financial strain is ongoing, lenders may agree to:

- Adjust interest rates

- Restructure payment schedules

- Change due dates

This is more likely when supported by documentation.

Voluntary Surrender (As a Last Resort)

If keeping the asset is no longer viable, voluntary surrender:

- May reduce fees

- Shows cooperation

- Can limit further damage

While not ideal, it can be better than forced repossession.

Step Four: Consider Refinancing or Selling the Asset

Refinancing

If your credit profile allows, refinancing may:

- Lower monthly payments

- Improve cash flow

- Prevent default

This option works best before repossession proceedings begin.

Selling the Asset

If the asset’s value exceeds the loan balance:

- Selling it yourself may preserve equity

- Prevent repossession

- Reduce credit damage

Timing is critical—once repossession occurs, control is lost.

Step Five: Understand the Credit Impact

Repossession and Your Credit Profile

Repossession can:

- Remain on credit reports for years

- Lower credit scores significantly

- Increase future borrowing costs

Stopping repossession—even after missed payments—often results in less long-term damage.

Damage Control Still Matters

If repossession cannot be avoided:

- Communicate with the lender

- Confirm balances and fees

- Understand deficiency obligations

Managing the aftermath responsibly helps recovery.

Applying a CEO Mindset to Repossession Risk

Treat Assets Like Business Assets

Businesses monitor asset utilization and financing carefully. Apply the same discipline personally:

- Avoid over-leveraging

- Match payment obligations to stable income

- Maintain liquidity buffers

Build Financial Resilience Going Forward

To reduce future risk:

- Maintain an emergency fund

- Avoid relying on minimum payments

- Regularly review cash flow

- Adjust obligations as income changes

Repossession prevention is not just about today—it’s about system design.

When Professional Help Is Appropriate

Credit Counselors and Financial Advisors

Professionals can:

- Review contracts

- Negotiate on your behalf

- Design sustainable repayment plans

Seek advisors focused on education and long-term outcomes.

Legal Guidance

In complex cases or disputes, legal advice may help clarify rights and responsibilities under local laws.

Conclusion

Stopping repossession is possible—but it requires speed, honesty, and strategy.

From a CEO-level perspective, repossession is a signal—not a sentence. It highlights a cash-flow imbalance that can often be corrected with decisive action and clear communication.

Key takeaways:

- Act early to preserve options

- Communicate proactively with lenders

- Understand your rights and contracts

- Choose realistic solutions over emotional reactions

Financial setbacks do not define leadership.

How you respond to them does.

With the right approach, you can protect your assets, stabilize your finances, and move forward with confidence.

Summary:

The threat of repossession is a real one to many people. When the economy is good, mortgage lenders are willing to lend many times your salary at low interest rates. If interest rates rise, however, or your experience job loss, sickness, divorce or other circumstances that reduce your income, you could find yourself in mortgage trouble.

Once your mortgage company has started repossession proceedings, it�s easy to give in and let the court process take its course, but there…

Keywords:

Article Body:

The threat of repossession is a real one to many people. When the economy is good, mortgage lenders are willing to lend many times your salary at low interest rates. If interest rates rise, however, or your experience job loss, sickness, divorce or other circumstances that reduce your income, you could find yourself in mortgage trouble.

Once your mortgage company has started repossession proceedings, it�s easy to give in and let the court process take its course, but there are ways that you can slow down and even stop the repossession process:

- Talk to your mortgage company

Even at the last minute, it�s possible to work out a deal with your mortgage company. Whether it�s raising additional money to clear your debts, or just agreeing a new payment plan, your mortgage company should be willing to come to an agreement with you. Don�t think that because you have been given a date for the courts to consider a repossession order that you don�t have time to sort things out.

- Be prepared

If you do have to go to court, make sure you are fully prepared. Keep copies of all the letters and other correspondence you have had with the mortgage company, work out a detailed daily expenditure that shows where you can save money so that you can begin paying your debts and be ready to explain to the court why you are in payment difficulties in the first place. The court may grant an adjournment or delay the repossession order if you can show that you are prepared to take your financial responsibilities seriously.

- Seek advice

If you are in danger of losing your home to the mortgage company, then take legal and financial advice to ensure that you are doing everything possible to avoid repossession. A good legal adviser will make sure that the mortgage company is following due process and not making it unreasonably difficult for you to make payments and clear your debts. They can also help you if you need to go to court, explaining the process and making sure that you have all the supporting documentation you need.

A specialist financial adviser can arrange short-notice loans, which can help you to get out of trouble. With just a few days notice and with access to dedicated lenders, they can arrange a loan that allows you to pay off your debts and start afresh. They can also arrange a quick house sale, without the need for estate agents fees or a lengthy sales procedure, which means that you raise the money you need with the minimum hassle.

Tinggalkan Balasan