Saving money is one of the most important steps toward financial freedom, yet it can feel daunting in a world full of expenses, debt, and financial temptations. Whether your goal is building an emergency fund, investing for the future, buying a home, or simply reducing stress, saving money requires strategy, discipline, and smart habits.

This guide explores actionable ways to save money, explains why saving is essential, and provides strategies for all income levels, helping you take control of your finances today.

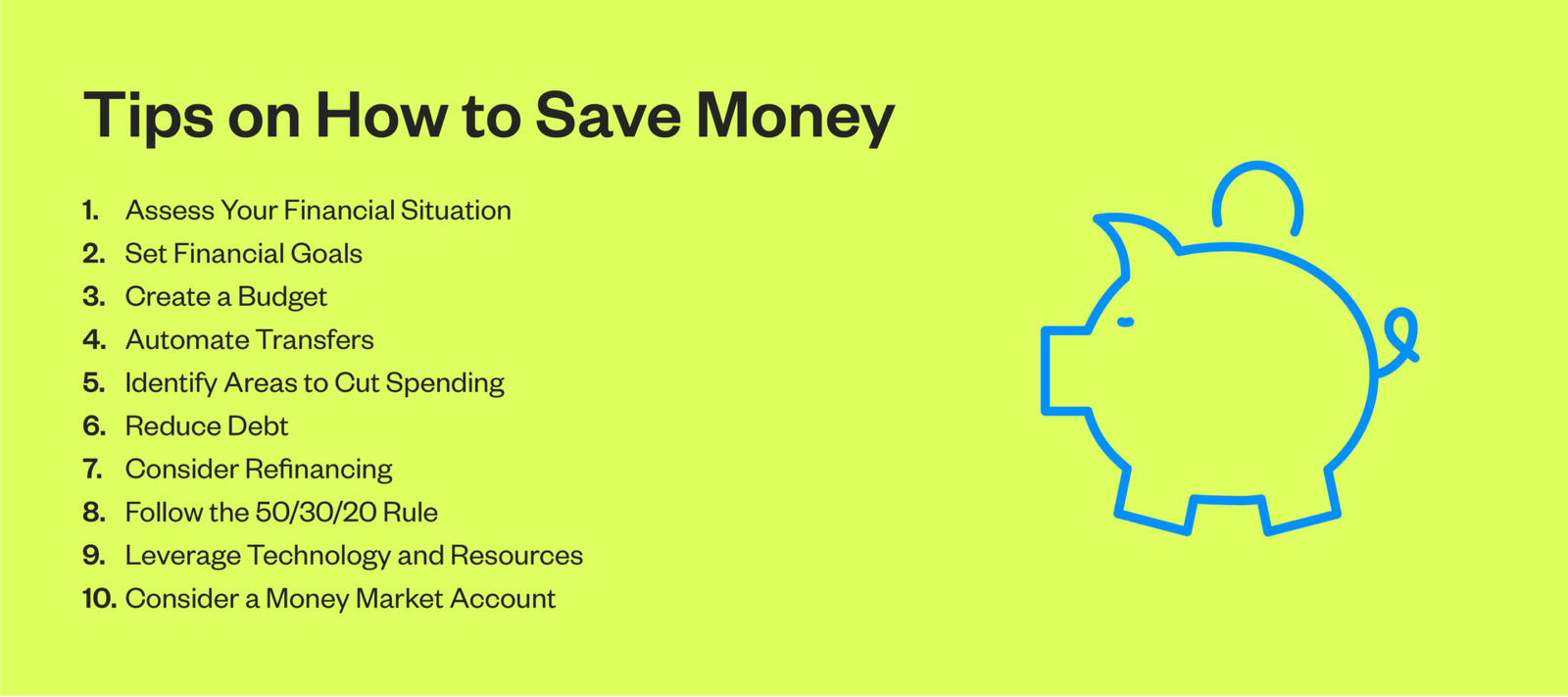

1. Why Saving Money Matters

a. Financial Security

- Savings provide a safety net for emergencies such as medical bills, car repairs, or job loss.

- Reduces dependence on high-interest debt like credit cards or payday loans.

b. Achieving Goals

- Buying a home, starting a business, traveling, or funding education often requires accumulated savings.

- Goals are more achievable when you plan and save consistently.

c. Reducing Stress

- Financial uncertainty is a major source of stress.

- Knowing you have funds available provides peace of mind.

d. Building Wealth

- Savings can be invested to grow over time, increasing your net worth and long-term financial freedom.

2. Start with a Budget

The foundation of any savings plan is knowing where your money goes.

a. Track Your Income and Expenses

- List all income sources: salary, freelance work, investments.

- Record all expenses: rent/mortgage, groceries, bills, subscriptions, discretionary spending.

b. Categorize Expenses

- Essential: Housing, utilities, groceries, transportation.

- Discretionary: Dining out, entertainment, hobbies.

- Savings: Emergency fund, retirement, investments.

c. Use the 50/30/20 Rule

- 50% for needs

- 30% for wants

- 20% for savings and debt repayment

Budgeting helps identify areas where you can cut costs and prioritize saving.

3. Build an Emergency Fund

An emergency fund is a financial cushion for unexpected events.

a. How Much to Save

- Ideally, save 3–6 months of living expenses.

- Even a small emergency fund can prevent reliance on high-interest debt.

b. Where to Keep It

- High-yield savings accounts or money market accounts for liquidity and modest interest growth.

c. How to Contribute Consistently

- Automate transfers each payday.

- Start small if necessary—$50–$100 per month adds up over time.

4. Reduce Everyday Expenses

Cutting unnecessary spending can dramatically increase savings.

a. Track Subscriptions

- Cancel unused services like streaming, apps, or gym memberships.

b. Shop Smart

- Use coupons, cashback apps, and price comparison tools.

- Buy generic brands for groceries and household items.

c. Reduce Utility Bills

- Turn off unused lights, unplug electronics, and consider energy-efficient appliances.

d. Cook at Home

- Preparing meals at home saves money and improves nutrition.

e. Limit Impulse Purchases

- Wait 24–48 hours before major purchases to avoid buyer’s remorse.

5. Automate Your Savings

Automation makes saving easier and consistent.

- Set up automatic transfers from checking to savings accounts.

- Automate retirement contributions through your employer.

- Treat savings like a recurring bill—pay yourself first.

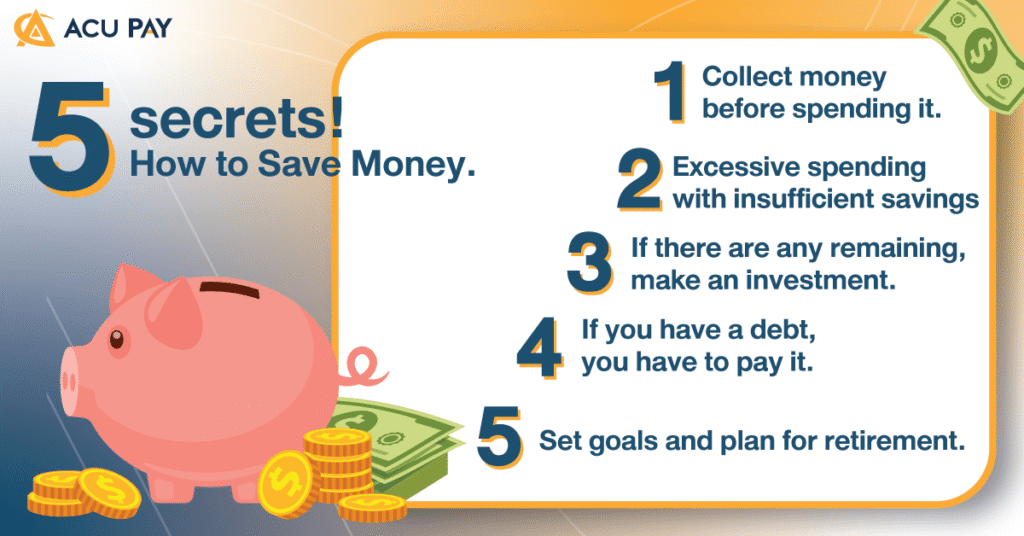

6. Pay Down High-Interest Debt

Debt often undermines savings. Focusing on repayment increases your financial flexibility.

a. Prioritize High-Interest Debt

- Credit cards and payday loans often have the highest interest rates.

- Pay more than the minimum when possible.

b. Debt Snowball vs. Debt Avalanche

- Debt Snowball: Pay smallest debts first for psychological motivation.

- Debt Avalanche: Pay highest-interest debts first to save the most money.

c. Consolidate Debt Wisely

- Consider a personal loan or balance transfer credit card to reduce interest rates.

7. Save on Big-Ticket Items

Major expenses require strategic planning:

a. Housing

- Downsize or refinance to lower monthly payments.

- Compare insurance providers to reduce costs.

b. Transportation

- Use public transport, carpool, or consider buying a reliable used car instead of a new one.

- Maintain vehicles properly to prevent costly repairs.

c. Education

- Use scholarships, grants, or employer tuition reimbursement programs.

- Compare student loans and repayment terms carefully.

d. Travel and Vacations

- Book flights early, use rewards points, and travel during off-peak seasons.

8. Maximize Income Opportunities

Increasing income helps accelerate savings:

- Freelance or side hustles

- Selling unused items online

- Renting out a spare room or parking space

- Negotiating salary increases or bonuses

9. Take Advantage of Financial Tools

a. High-Yield Savings Accounts

- Earn more interest compared to traditional accounts.

b. Certificates of Deposit (CDs)

- Secure savings for a fixed term with guaranteed returns.

c. Investment Accounts

- Stocks, mutual funds, or ETFs can grow wealth over time.

- Ensure risk aligns with your goals and timeline.

d. Budgeting Apps

- Tools like Mint, YNAB, or personal spreadsheets help track spending and progress.

10. Adopt a Saving Mindset

Money-saving is not just about numbers—it’s a mindset:

- Set clear goals: emergency fund, vacation, retirement, or home purchase.

- Track progress to stay motivated.

- Celebrate milestones without overspending.

- Avoid lifestyle inflation as income rises.

11. Case Studies

Case Study 1: Small Changes, Big Impact

Emma started saving $100 per month by reducing dining out and subscriptions. Within a year, she had $1,200 in an emergency fund, giving her peace of mind and reducing reliance on credit cards.

Case Study 2: Side Hustle Savings

John freelanced on weekends and directed all earnings to savings. Over two years, he accumulated $15,000, enough for a down payment on a condo.

Case Study 3: Debt Reduction Boosting Savings

Sarah focused on paying off a high-interest credit card while automating $50/month into savings. Once debt was cleared, she redirected payments to her emergency fund, accelerating her financial security.

12. Common Mistakes to Avoid

- Failing to Budget: Without tracking, money slips away unnoticed.

- Ignoring Small Expenses: Daily coffees and snacks add up.

- Overreliance on Credit: Borrowing instead of saving creates a cycle of debt.

- No Emergency Fund: Unexpected expenses force reliance on high-interest loans.

- Not Automating Savings: Without automation, saving is inconsistent.

13. Long-Term Saving Strategies

a. Retirement Accounts

- Contribute to 401(k)s, IRAs, or similar accounts.

- Employer matching programs are essentially free money.

b. Investment Planning

- Diversify investments to grow wealth steadily.

- Start early to benefit from compounding interest.

c. Financial Education

- Regularly read, attend seminars, or consult financial advisors.

- Knowledge improves decision-making and reduces financial stress.

14. Key Takeaways

- Saving money provides security, reduces stress, and builds wealth.

- Start with budgeting and tracking expenses.

- Build an emergency fund to cover unexpected costs.

- Reduce discretionary spending and high-interest debt.

- Automate savings and maximize income opportunities.

- Adopt a long-term mindset focused on consistent growth.

15. Conclusion: Saving Money is a Journey, Not a One-Time Task

Saving money is not a single action—it’s a lifestyle and mindset. By combining budgeting, disciplined spending, debt management, and smart financial tools, anyone can take control of their finances.

Even small, consistent actions add up over time, providing financial security, freedom, and peace of mind. Whether your goal is short-term stability or long-term wealth, the principles outlined in this guide create a roadmap to save effectively and build a better financial future.

Remember: the journey to financial security starts with one step—start today, and let your savings grow steadily over time.

Summary:

If you’re asking “how can I save money?”, then this article is for you! You have to do something different than you’re doing now. So let Leo Quinn give you some great tips for figuring out how much to save, where to save, when to save and how to get someone to do it all for you!

Keywords:

how do i save money, save money

Article Body:

Copyright 2006 Leo J Quinn Jr Enterprises, LLC

You’re probably reading this article because you really want to know: “How can I save money?”.

That means you probably aren’t a saver…you’re likely a spender.

Unfortunately, if you aren�t already a saver, then you have little chance of developing a saver�s mentality.

There are always exceptions, of course, but you are either a saver or a spender, and for most folks, no matter how hard they try, they�ll never be able to change.

And you know what? There�s nothing inherently wrong with either (unless you take it to extremes, of course). It has a lot to do with your God-given personality.

So, if you�re a spender, not a saver, accept the way you are. Acknowledge your weakness. Say, out loud:

�I am a spender, not a saver. I know I should save more. I will find a way to save more and plan for my future.�

Now, develop a plan to overcome your weakness, one that doesn�t involve changing who you are! (Because we both know that�ll never happen.)

Accept the fact you will have to do a couple things that may be unpleasant to you, for various reasons:

- Figure out what you earn and what you spend

- Adjust spending until you reach your desired savings amount

- Decide how much you will save, and with what vehicle (401(k), Roth IRA, traditional IRA, high-yield savings account, brokerage account, etc.)

But wait! If you know there is no way you�ll ever do these things, then find someone who enjoys doing them, and hire them to do it for you. Problem solved!

Now, all you have to do is turn over your information, and wait for the report.

Don�t be foolish, though. Before hiring help, make sure you find:

- Someone you can trust with your personal financial data

- Someone who charges on a fee basis only

- Better yet, someone who might be willing to barter services with you

Now, decide on a reward you will give yourself when you have completed the your tasks (or hired someone else to). What will it be? A night at the movies? A bubble bath? A new CD? Make it something you really, really want.

All done? Good. Enjoyed your reward? Great.

Take the final step to guarantee you�ll be a saver forever:

Set up automatic withdrawals from your checking account to your savings vehicles for the amounts you need to save.

That�s it. That�s all there is to it.

You already know how much you can save. You know where you want to save it.

Just set it up to run every week, paycheck, month, quarter�whatever works for you!

Go to the websites. Go to the Human Resources representative that can help you with paperwork. Pick up the phone. Just do it.

Now, plan your reward for completing this final, all-important task. Make it worthwhile.

Again, if you feel you�d never complete this task regardless of how much you want to save, hire someone to do it for you! They�ll know your user ID�s and passwords, so you may want to change those once the setup is complete.

The point is, what you�re doing now doesn�t work. Unless you completely change your tendencies, you�ll never do what you know you should�save some, or more, money. So you MUST do something different!

Why not try this?

Once your system is set up, you will have nothing left to do but spend whatever money is left over! Your savings are in place, and you�ll get used to not having that money, because you never see that money.

And when your statements arrive in the mail showing how much you�ve saved and/or invested, you�ll be thrilled!

Not everyone is a saver. But everyone can save!

Now go to it.

Tinggalkan Balasan